High-Low Method: Learn How to Estimate Fixed & Variable Costs

The high-low method is a straightforward, if not slightly lengthy, way to figure out your total costs. Fixed costs are expenses that remain the same irrespective of the quantity or number of units of goods produced for sale or services rendered. The high-low method can be done graphically by plotting and connecting the lowest point of activity and the highest point of activity.

Advantages and disadvantages of the high-low method accounting formula

The high-low method may produce inaccurate results since it only considers two extreme data points, which may not be representative of other data points. It can also be unreliable because it’s possible that the highest and lowest points are outliers. For the months from June to August, the actual costs are always higher than the computed costs. These variances can stem from different causes, and every business manager should look at the variances. To substitute the rest except a, we pick either the high or low point as reference. Nevertheless, it has limitations, such as the high-low method assumes a linear relationship between cost and activity, which may be an oversimplification of cost behavior.

High-low Method in Accounting: Definition, Formula & Example

The following are the given data for the calculation of the high-low method. For example, the table below depicts the activity for a cake bakery for each of the 12 months of a given year. Take your learning and productivity to the next level with our Premium Templates.

Ask Any Financial Question

Studies arising from HICs (as defined by a Human Development Index value of ≥0.700 [18] at the median year of data collection) must have at least 200 patients included in the study to increase the probability that at least one death may be recorded in the study. This requirement will be waived for LMICs due to the anticipated sparsity of data. Conditions requiring surgical treatment are highly prevalent worldwide, and unmet need for surgery accounts for approximately one-third of the global burden of disease [1–3].

Step 2: Calculate the Variable Cost Per Unit

- This eventual study may help policymakers and other key stakeholders with benchmarking surgical safety initiatives as well as identify key gaps in our current understanding of global perioperative mortality.

- This article describes the high-low method formula and how to use the high-low cost method calculator to estimate any business or production cost per unit.

- The fixed cost can be calculated once the variable cost per unit is determined.

- Unfortunately, the only available data is the level of activity (number of guests) in a given month and the total costs incurred in each month.

- But more importantly, this scenario shows the weakness of the high-low method.

- This is another advantage for this study to help reduce confounding and account for unexplained variation between studies [30].

In our previous dog groomer example we could clearly see through our scattergram that maintenance costs were related to the number of dogs groomed. Remember that that was our initial diagnostic step before we moved on to more detailed analysis of our costs. Data x represents the number of units while y represents the corresponding cost. Due to its unreliability, high low method should be carefully used, usually in cases where the data is simple and not too scattered.

Follow the steps below to perform the high-low method by using our sample data from Fusion Company. Let’s assume that the company wants to project client support costs for next year’s budgeting. The company claiming the making work pay tax credit plans to produce 7,000 units in March 2019 on the back of buoyant market demand. Help the company accountant calculate the expected factory overhead cost in March 2019 using the high-low method.

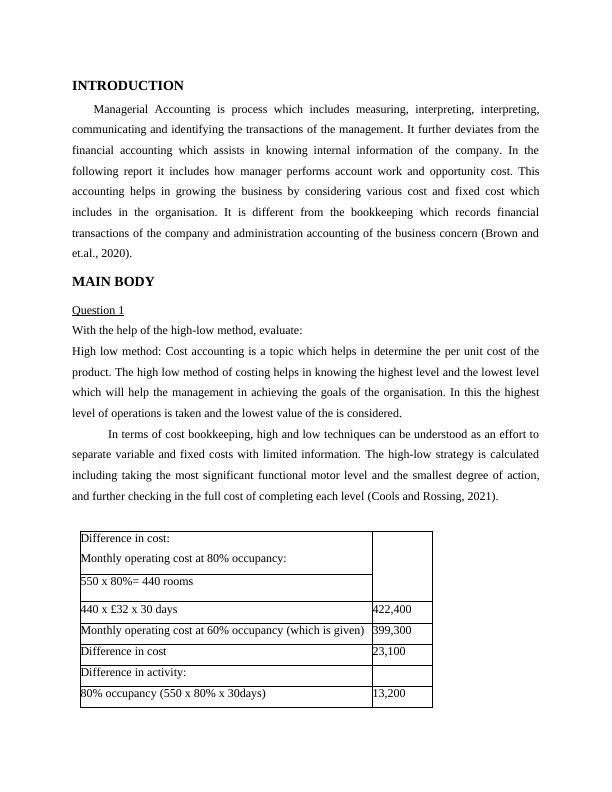

The high-low method involves taking the highest level of activity and the lowest level of activity and comparing the total costs at each level. The high-low method is a cost accounting technique that compares the total cost at the highest and lowest production level of business activity. It uses this comparison to estimate the fixed cost, variable cost, and a cost function for finding the total cost of different production units. In cost accounting, the high-low method formula refers to the mathematical technique used to separate fixed and variable components that are otherwise part of the historical cost that is mixed, i.e., partially fixed and partially variable.

Among the proposed metrics to capture data regarding the progress of establishing universal access to safe and affordable surgery POMR stands alone as the sole measure of patient safety. As such it is important for health systems to understand both the current rate of perioperative mortality as well as where such a rate fits into the broader historical trends. The secondary objective is to investigate cause-specific mortality in an attempt to understand the causes driving POMR. Data on causes will first be presented as overall proportions aggregated by type of surgery, time and HDI category wherever possible. Sankey diagrams will be used to better visualize changes over time in these proportions to provide a clearer picture of the impact of the causes on perioperative mortality.

Related Articles

Categories

- ! Без рубрики 623

- "qaladiza Wikipedia – 250 5

- 0,01577823422 1

- 0,04107633464 1

- 0,04744125425 1

- 0,05760432875 1

- 0,0583320658 1

- 0,08791713633 1

- 0,1015940489 1

- 0,1068716727 1

- 0,1334400616 1

- 0,1409452317 1

- 0,1428694182 1

- 0,1537627118 1

- 0,1621577533 2

- 0,1781118702 1

- 0,1927127078 2

- 0,1952114739 1

- 0,2214654612 1

- 0,2553001222 1

- 0,2604054412 1

- 0,2730889835 1

- 0,2796021684 1

- 0,3008005281 1

- 0,3195203253 1

- 0,3201181085 1

- 0,3422332539 1

- 0,3573748986 1

- 0,3755073542 1

- 0,3895651081 1

- 0,4099923332 2

- 0,4196563314 1

- 0,5388359029 1

- 0,5472184121 1

- 0,5489275351 1

- 0,5667208347 1

- 0,5718359556 1

- 0,5801122156 1

- 0,5808754638 1

- 0,5826764591 1

- 0,584460229 1

- 0,5882169779 1

- 0,5893577013 1

- 0,6247481116 1

- 0,627540254 1

- 0,6496948061 1

- 0,7028154566 1

- 0,7139460789 2

- 0,7203799266 1

- 0,7241439169 1

- 0,7864154417 1

- 0,7870634885 1

- 0,7919928325 1

- 0,8546404277 1

- 0,8706533551 1

- 0,8759138712 1

- 0,878152494 1

- 0,8839889182 1

- 0,8893974138 1

- 0,906819777 1

- 0,9166982236 1

- 0,919269795 1

- 0,9309246699 1

- 0,9449587806 1

- 0,9804490622 1

- 0,9953594 1

- 08. goldstueck-vienna.at 1

- 09. ArmesTheaterWien.at 1

- 09.12 1

- 1 176

- 1 Win Aviator 1

- 1-win.co.mz z1 1

- 10 Euro Slottica Casino Bonus Best Online Casino Site – 619 4

- 10 parasta postimyyntiä morsiamen 1

- 1000 50-50 allZ 4

- 1000 allZ 4

- 1000 ancorZ 11

- 10000_tr 1

- 10000_wa 3

- 10000_wa2 1

- 10000sat 2

- 10000sat2 2

- 10000sat5 2

- 10000sat7 1

- 10005sat 2

- 10050sat 1

- 10050tr 2

- 10060_wa 2

- 10065_wa 1

- 10100_sat2 1

- 10100_tr 1

- 10110_sat 2

- 10150_sat 2

- 10150_tr 4

- 10200_sat 1

- 10200_sat2 1

- 10200_tr 2

- 10200_wa2 3

- 10210_wa 1

- 10250_prod 1

- 10250_wa 1

- 10260_sat 1

- 10300_wa 3

- 10300sat 1

- 10350_sat 1

- 10390_sat 1

- 10400_prod2 3

- 10400_prod3 2

- 10400_sat 2

- 10450_wa 1

- 10480_sat 2

- 10500_sat 2

- 10500_sat2 2

- 10500_sat3 1

- 10500_wa 1

- 10500_wa2 1

- 10510_tr 2

- 10510_wa 1

- 10525_sat 2

- 10550_sat 2

- 10550_sat2 2

- 10600_prod2 2

- 10600_sat 2

- 10600_sat2 2

- 10600_tr 1

- 10650_tr 2

- 10655_pr 1

- 10700_pr 1

- 10700_sat 2

- 10700_wa 1

- 10700_wa2 1

- 10800_tr 2

- 10800_wa 2

- 10831_wa 1

- 10850_sat 1

- 10985_wa 2

- 11 2

- 1100 links Turkey Casino 1

- 11000prod3 2

- 111 1

- 112 1

- 1126 1

- 11380_wa 1

- 11800_prod 1

- 14 1

- 1581i 2

- 1650 links English Casino 1

- 188bet Mobile: Nền Tảng Cá Cược Tốt Nhất Việt Nam – 562 4

- 1bet5 1

- 1GullyBet 1

- 1win App 48 1

- 1win Casino Argentina 6 1

- 1win Casino Chile 412 3

- 1win-azerbaycan.az 1

- 1winazerbaycan.org 1

- 1wins-moldova.mdro-md x1 1

- 1xbet Games 48 3

- 1xbet-1 1

- 1xbet-2 1

- 1xbet-6 1

- 1xbet-bangl.com 1

- 1xbet-malaysia.com 2

- 1xbet-online-casino.com 1

- 1xbet-online-casino.comuz 1

- 1xbet-royxatdan-otish.com 1

- 1xbet-uzbek.org 2

- 1xbet1 7

- 1xbet2 6

- 1xbet3 4

- 1xbet3231025 1

- 1xbet4 6

- 1xbet5 1

- 1xbet6 2

- 1xbet7 2

- 1xBetBangladesh 1

- 1xbetindonesia.id 1

- 1xbetmalaysia.com 1

- 1xcinta.org 1

- 1xlogin.com 1

- 1xslot.beregaevo.ru 4-8 1

- 1xslots-casino-online.ru 4-8, 10 1

- 1xslots-oficialnyy-sayt.ru 4-8, 10 1

- 1xslots-vhod-zerkalo.ru 4-8, 10 1

- 2 28

- 20 Bet Casino 216 3

- 20 Bet Casino 978 3

- 2000 ancorZ 1

- 20bet App 551 3

- 20bet Bonus 616 1

- 20bet Casino 299 3

- 20bet Casino Logowanie 104 3

- 20bet Casino Logowanie 982 3

- 20bet Kasyno 371 1

- 20bet Login 681 3

- 20bet schweiz 1

- 20betschweiz.ch 1

- 21 1

- 220 links Switzerland Crypto 1

- 2200 links Thailand Casino 2

- 222 2

- 24 1

- 25. mukusal.at 1

- 2520 links UK Casino 1

- 26 2

- 26. gasthof-kasern.at 1

- 27. salzburgtv.at 1

- 28. hackthecrisis.at 1

- 3 8

- 3. planungundvielfalt.at 1

- 30 1

- 30. rudolfhundstorfer.at 1

- 31 2

- 32 1

- 3240 3

- 330 links USA Ai headshot 1

- 350 links Korea 1

- 3569 4

- 365betaustria.at 1

- 365betofficial.com 1

- 3Ziko.pl 1

- 4 3

- 40-burning-hot-6-reels.gr 1

- 4rabet Bonus 953 1

- 4rabet-app.com 1

- 5 7

- 5-7 1

- 5. nobelvienna.at 1

- 5.agorascienza 1

- 50-50 500 2

- 50-50 allZ 3

- 500 50-50 allZ 8

- 550 links English Casino 1

- 554i 1

- 6 4

- 660 links Brazil Casino 1

- 660 links Turkey Casino 1

- 7 2

- 7 Slottica 7 Mobilna Zarejestruj Się – 851 1

- 70-30 1000 16

- 70-30 allZ 10

- 7777777 1

- 77777777 1

- 777777777 1

- 7slots TR 1

- 8 2

- 8550_tr 2

- 9030_wa 1

- 9110_wa 1

- 9220_wa 1

- 924 1

- 9440_prod 1

- 9600_sat2 1

- 9600_wa 1

- 9700_sat 1

- 9700_sat2 1

- 9760_sat 1

- 9800_wa 1

- 9900_sat 1

- 9900_sat2 1

- 9900_wa 1

- 9925_sat 1

- 9950_prod 1

- 9950_tr 1

- 9950_wa 1

- 9985_sat 1

- 9990sat 4

- 9bet-brazil.com 1

- a legitimate mail order bride 6

- a mail order bride 8

- är postorder brud säker 1

- a16z generative ai 3

- a16z generative ai 1 1

- abstraktdergi.net 2000 1

- Abuking.info 14

- Abukingcasino-fr.fr 1

- accionmad.org 1

- accionmad.org_casino-online-europa 1

- acheter une mariГ©e par correspondance 2

- achterafbetalen 1

- Admin 2

- adobe generative ai 1 3

- adobe generative ai 2 1

- adobe generative ai 3 2

- afyonsosyetepazari.com 1 1

- Agence de messagerie de commande de mariГ©e 6

- Agence de vente par correspondance avec la meilleure rГ©putation 4

- Agences de la mariГ©e par correspondance 2

- agences de mariГ©e par correspondance 2

- agencia de novias por correo 1

- agencias de novias por correo 1

- Agencija za mail za mladenku 1

- agenzia di posta per ordini di sposa 2

- agenzia sposa per corrispondenza 1

- AI in Cybersecurity 1

- airsoftparadise.cl 1

- akkordeonfest.ch 1

- aldeauruel.com.ar c1 1

- alexandraharney 1

- aliexpressofficial.com 1

- alll 1

- allyspin-casino.at 1

- Allyspin-casino.net 2

- Allyspinkasyno.pl 3

- almaradio.gr 1

- Almarokna 1

- Almissa.org 2

- Alpaguesthouse.it 1

- ambridgeevents.com 1

- amex 1

- amminex.net 2 1

- amnistiepdm.org – Official Website of Safe Casino Sites in South Korea 1

- Amunracasino-si.com 1

- Amunracasino.info 1

- Analytics 1

- anbhoth.ie 1

- ancor100 1

- ancorallZ 5

- ancorallZ 1000 34

- ancorallZ 10000 5

- ancorallZ 1200 1

- ancorallZ 1250 4

- ancorallZ 130 1

- ancorallZ 1310 1

- ancorallZ 1400 5

- ancorallZ 145 1

- ancorallZ 150 1

- ancorallZ 1500 50

- ancorallZ 15000 3

- ancorallZ 15000TR2 7

- ancorallZ 1610 9

- ancorallZ 17500TR2 4

- ancorallZ 180 4

- ancorallZ 185 1

- ancorallZ 2000 62

- ancorallZ 2000_2 1

- ancorallZ 220 2

- ancorallZ 250 1

- ancorallZ 2500 1

- ancorallZ 275 1

- ancorallZ 2800 1

- ancorallZ 300 12

- ancorallZ 3000 18

- ancorallZ 3000s 4

- ancorallZ 308 5

- ancorallZ 350 2

- ancorallZ 480 1

- ancorallZ 50% 8

- ancorallZ 500 15

- ancorallZ 600 2

- ancorallZ 700 4

- ancorallZ 75 1

- ancorallZ 800 2

- ancorallZ 900 1

- ancorallZ 900 5

- ancorallZ 9000 3

- ancorallZ TP2 1

- ancorallZ201 1

- ancorZ 1500 2

- ancorZ 2500 15

- ankaratarotfali.com 2 1

- anmeldelser av postordrebrudbyrГҐ 2

- antalyaerenhali.com 1 1

- antikaeltehilfe.de 1

- Apex legends cheats 1

- apoteka1 1

- applepaycasinos 1

- approveit 1

- aprofi34.ru 1000 1

- ar-bcgame 1

- arbelecos.es 2

- armynow.net 1

- articles 35

- Articles de la mariГ©e par correspondance 1

- Arts & Entertainment, Music 2

- artГculos de novia por correo 1

- Asino.casino 3

- Asino.club 1

- Asino.pro 1

- asv-wohlen.ch 1

- atlantikcorner.com 1

- AU Casino 1

- auenrietheim.ch 1

- Auf der Suche nach einer Mail -Bestellung Braut 1

- augustent.com 1 1

- Auslandische Brute 2

- Australia Casino 1

- Australia Casino1 1

- auto-info.hr 2 1

- autokarossrescue.se 1

- average age of mail order bride 2

- average cost of a mail order bride 2

- average cost of mail order bride 5

- average mail order bride prices 4

- average price for a mail order bride 4

- average price for mail order bride 2

- average price of a mail order bride 5

- average price of mail order bride 6

- Avia 1

- avia masters 1

- aviator 1

- Avis des mariГ©es par correspondance 1

- Avis sur le site Web de la commande par correspondance 1

- avito-club.ru 100 1

- Avocasino-pt.com 1

- awardhealthandsafety 1

- axiomaltd.ru 1500 2

- az-melbet 1

- aze-1xbet 1

- aze-mostbet 1

- Azer Casino 2

- Azer Casino2 1

- azer1xbet 2

- Azerb 1

- Azerbaycan Casino 1

- Azerbaycan Casino1 1

- azpinupcasino 1

- Azr Casino 1

- azsportline.com 1

- bästa land att hitta postorder brud 1

- bästa landet att hitta en postorderbrud 2

- bästa platser för postorderbrud 1

- bästa postorder brudens webbplats 1

- bästa postorder brudföretag 1

- bästa riktiga postorder brud webbplats 2

- bästa rykte postorder brud 1

- bästa stället att få en postorderbrud 1

- bästa webbplats för att hitta en postorderbrud 1

- bästa webbplats postorder brud 1

- babu88-bangladesh.net 1

- baji999-bd.net 1

- bambturkiye.com 1 1

- bancorallZ 100 2

- bancorallZ 1000 2

- bancorallZ 120 12

- bancorallZ 1200 1

- bancorallZ 1250 3

- bancorallZ 1500 1

- bancorallZ 200 1

- bancorallZ 500 10

- bancorallZ 585 1

- bancorallZ 800 1

- bancorallZ TP2 15000 5

- bancorallZ TP215000 3

- bancorZ 2500 9

- barceloneta-dresden.de 1

- barnmatsbutiken.se 1

- bashpirat.ru 2000 1

- basicallyjohnnymoped.com 1

- bass-bet-casino.at 1

- bassbet-bonus.at 1

- bassbetofficial.com 1

- batery.org.in4 1

- bating9 2

- bauhutte-g.com 1

- BC Game Casino 1

- bc-fun-mirror.com 1

- bc-game-uae.com 1

- bc-game.ph 1

- bc-games-ng.com 1

- bc-hashgame.com 1

- bc5 1

- bcg4 2

- bcg5 1

- bcgame-casino-au.com 1

- bcgame-cryptobet.com 1

- bcgame-play-ph.com 1

- bcgame-playcasino.com 1

- bcgame1 14

- bcgame2 13

- bcgame3 11

- bcgame4 6

- bcgame5 2

- bcgame6 4

- bcgame7 1

- Bdmbet Application 40 1

- Bdmbet Casino Avis 139 3

- beach5.ch 1

- beach5.ch_betonred 1

- bedava-slot.com 1500 1

- bedwinner1 1

- Beep-beep.casinologowanie.net 1

- beethecity 1

- beregaevo.ru 4-8 1

- beregaevo.ru ancorallZ 180 1

- Beritabawean.com 2

- berkeleycompassproject2 1

- berkeleycompassproject3 1

- bessemercitymiddleschool.com 1

- BEST bewertete Versandauftragsbrautseiten 2

- best countries for a mail order bride 2

- best countries to get a mail order bride 3

- best country for mail order bride 3

- best country for mail order bride reddit 7

- best country to find a mail order bride 3

- best country to find mail order bride 4

- best essay cheap writer 1

- best legit mail order bride websites 2

- best mail order bride 5

- best mail order bride agency 5

- best mail order bride agency reddit 5

- best mail order bride companies 6

- best mail order bride company 5

- best mail order bride countries 7

- best mail order bride country 4

- best mail order bride ever 1

- best mail order bride places 3

- best mail order bride service 6

- best mail order bride site 6

- best mail order bride site reddit 8

- best mail order bride sites 6

- best mail order bride sites reviews 2

- best mail order bride website 2

- best mail order bride websites 3

- best mail order bride websites 2022 3

- best mail order bride websites reddit 3

- best place for mail order bride 5

- best place to get a mail order bride 3

- best place to get mail order bride 7

- best places for mail order bride 3

- best places to find mail order bride 4

- best places to get mail order bride 4

- best rangerte postordrebrudesider 1

- best rated mail order bride sites 3

- best real mail order bride site 7

- best real mail order bride sites 7

- best reputation mail order bride 5

- best site mail order bride 3

- best website to find a mail order bride 5

- best-news 2

- best-tr-casinos 1

- bestappstrading 1

- bestbinary 1

- bestbrokercfd 1

- bestbrokercfd.com 1

- bestdiplomsa.com 1

- Beste echte Mail -Bestellung Brautseite 1

- Beste echte Mail -Bestellung Brautseiten 2

- beste ekte postordre brud nettsteder 1

- beste ekte postordre brudeside 1

- beste land for postordrebrud 1

- beste landet ГҐ finne postordrebrud 2

- Beste Mail -Bestellung Braut 1

- Beste Mail -Bestellung Braut -Websites Bewertungen 9

- Beste Mail -Bestellung Braut aller Zeiten 2

- Beste Mail -Bestellung Braut Site Reddit 1

- Beste Mail -Bestellung Brautagentur 1

- Beste Mail -Bestellung Brautpletze 3

- Beste Mail -Bestellung Brautseite 2

- Beste Mail -Bestellung Brautseiten 1

- Beste Mail -Bestellung Brautunternehmen 2

- Beste Mail -Bestellung Brautwebsite 4

- Beste Mail -Bestellung Brautwebsites 2

- Beste Mail bestellen Braut Websites Reddit 3

- beste nettsted for ГҐ finne en postordrebrud 2

- beste nettsted for ГҐ finne en postordrebrud 1

- beste nettsted post ordre brud 4

- beste omdГёmme postordre brud 2

- Beste Orte, um Versandbestellbraut zu erhalten 1

- Beste Orte, um Versandbestellbraut zu finden 5

- beste postordre brud nettsted 1

- beste postordre brud nettsteder 3

- beste postordre brud nettsteder reddit 3

- beste postordre brud noensinne 1

- beste postordre brudbyrГҐ 2

- beste postordre brudebyrГҐ reddit 1

- beste postordre brudfirma 3

- beste postordre brudland 3

- beste postordre brudplasser 1

- beste postordre brudselskaper 2

- beste postordre brudtjeneste 1

- beste steder ГҐ fГҐ postordrebrud 2

- Beste Versandbestellung Braut Land 2

- Beste Versandbestellung Brautlender 2

- Beste Website, um eine Mail -Bestellung zu finden, Braut 2

- Bester Ort fГјr Versandbestellbraut 1

- Bester Ort, um Versandbestellbraut zu erhalten 3

- Bestes Land fГјr Versandbestellbraut Reddit 4

- Bestes Land, um eine Versandbestellbraut zu finden 3

- Bestes Land, um Versandbestellbraut zu finden 4

- besyohocam.com 2 1

- bet-1 1

- bet-13 1

- bet-andreas-india.com 1

- bet1 14

- bet13 1

- bet2 15

- bet20 1

- Bet20 Casino 844 3

- bet3 11

- Bet365 App Download 564 3

- Bet365 Official Global website 1

- Bet365 Schweiz Website 1

- bet365downloadapp.com 1

- bet4 7

- bet5 2

- bet6 1

- bet8 1

- bet9 1

- betandreas 1

- betandreas-azerbaijani.com 1

- betandreas-azerbaycani.com 1

- betandreas-now.com 1

- betandreas.co.in 1

- betandreas2 2

- betandreas3 1

- betandres-az.com 1

- betandres-kz.com 1

- Betano Pariuri 675 1

- betano-casino.gr – GR 1

- betanoaustria.at 1

- betanocasino.gr – GR 1

- Betbarter Casino 70 3

- betblastcasino.onlin 1

- betcasino1 2

- betcasino5 1

- Betesporte E Confiavel 232 3

- Betfiery Abertos Agora 283 1

- bethardofficial.se 1

- Beticocasino.net_July 1

- betify 2

- betine – hollypuffs.com 1

- betinfernocasino.se 2

- betkom- klasikotomobilmuzesi.net 1

- betmarathon-uz.com 1

- betmine.site 1

- betnano – sagliklihayat.net 1

- betoffice – ruyameali.com 1

- Betonred Promo Code 107 1

- betonredcasino.gr – GR 2

- betspecial.co.uk 2 1

- BETT 1

- betting 12

- betting5 1

- bettt 1

- betunlim.pt 1

- Betway Online 592 3

- betway-eg1.com 1

- betwinner 2

- betwinner-apk.net 1

- betwinner-bj.com 1

- betwinner-brasil.net 2

- betwinner-cm.com 1

- betwinner-franc.com 1

- betwinner-partner.com 1

- betwinner-turkish.com 1

- betwinner1 14

- betwinner2 16

- betwinner3 12

- betwinner4 3

- betwinner5 1

- betwinneregypt.com 1

- betzula – cerkezkoyevdenevenakliye.com 2

- Bewertungen zu NV Casino Schweiz 1

- bezflash.rugamesbrowseorder=newest 5 1

- bguzel.ru 20 1

- bhs 10

- bhs-bim 1

- bhs-seo 10

- bhs-teen 2

- Big Game Casino 226 1

- Bigclashkasino.de 1

- bilimufku.com 2000 1

- billybets.at 1

- Bir Gelin Bul 1

- Bir posta sipariЕџi gelini bulun 1

- Bir posta siparişi gelini için en iyi ülkeler 2

- Bir posta siparişi gelini için ortalama fiyat 1

- bir posta sipariЕџi gelini nasД±l evlenir 1

- Bir posta sipariЕџi geliniyle Г§Д±kmalД± mД±yД±m 1

- Bir posta sipariЕџinin ortalama fiyatД± 1

- biskotakimou.gr 1

- bitcasino-japan.com 1

- bitwinner2 1

- bizzocasino-greece.net – GR 1

- bla gjennom postordrebruden 3

- blog (1,405)

- bloomtiendas.com 1

- bocuci.ch 1

- BomerangBet 1

- bon site Web de mariГ©e par correspondance 1

- Bono Gratogana 92 3

- bons sites de mariГ©e par correspondance 2

- Bookkeeping 12

- Bookstime 1

- Boomerangcasino.info 1

- bootstrap-3.rucss.php 100 1

- borka.org.mk 1

- br 2

- br-2 1

- bra postorder brud webbplatser 1

- bra postorder brudens webbplats 1

- braintreerec.com2 1

- Brangocasino-nz.com 1

- Braut bestellen Mail 2

- Braut Weltversandbraut Braute 6

- Breaking News 9

- Breaking-News 3

- BreakingNews 1

- brend 1

- bride mail order 5

- BRIDE MAILLEMENT BRIDE Bonne idГ©e? 2

- bride order mail 3

- bride order mail agency 4

- bride world mail order brides 5

- Bride World Order Mail Brides 1

- Broad Spectrum Cbd Oil 748 3

- Broderiediamantpascher.fr 1

- browse mail order bride 2

- brucebet-casino.at 2

- brucepokiescasino 1

- brudebestillings mail 1

- brudens världs postorder brudar 3

- brudepostordre 2

- brunch-cafe.ru 1

- brut-club.ru 1500 1

- bubbleshop.ru 300 1

- buddhainstitute.in c2 1

- buen correo orden sitio web de la novia 2

- buenos sitios de novias por correo 2

- buitenlandsecasino 1

- buona posta elettronica siti sposa 1

- bus-shklyar.ru 500 1

- buscando matrimonio 1

- Business, Customer Service 1

- Business, Entrepreneurs 2

- Business, Marketing 1

- buy a mail order bride 4

- buy essay online for cheap 1

- buy mail order bride 10

- Buy Semaglutide 2

- buying a mail order bride 6

- bwinbet.ch 1

- CA Casino 2

- cambodia-1xbet.com 1

- camp-hockey.ru 500 1

- campionsbb.com 2000 1

- camposchicken.pe 2

- can i get a mail order bride if i am already married? 5

- can someone write an essay for me 1

- can you mail order a bride 3

- Canada Casino 2

- Canada Casino2 1

- Canada1 1

- cashbackcasinojp 1

- cashed-casino.eu.com – UK 1

- casiku-casino.fi – FI 1

- casikucasino.fi – FI 1

- casikucasino.uk – UK 1

- casino 215

- Casino Bdmbet 589 3

- Casino Bet365 471 3

- casino en ligne 1

- casino en ligne france 2 1

- casino en ligne luxembourg 1

- casino en ligne suisse legal 1

- casino online buitenland 1

- Casino Party 341 1

- casino review 2

- Casino Turkey11 1

- casino_online 3

- casino-1 1

- casino-10 1

- casino-12 1

- casino-13 2

- casino-15-11-1 2

- casino-16 1

- casino-17-11-1 1

- casino-18 1

- casino-19 1

- casino-20-11-1 1

- casino-25-11-1 1

- casino-4 1

- casino-5 1

- casino-6 1

- casino-7signs.gr – GR 1

- casino-8 1

- casino-9 1

- casino-bizzo-greece.com – GR 1

- casino-buran.gr – GR 1

- casino-casiny 1

- casino-funbet.gr – GR 1

- casino-goldenbet.fr – FR 1

- casino-joker8.gr – GR 1

- casino-malina.gr – GR 1

- casino-news 1

- casino-online 2

- casino-pistolo.de – DE 1

- casino-pistolo.fr – FR 1

- casino-quickwin.gr – GR 1

- casino-sevencasino.com 1

- casino-spinland.com 1

- casino-sugarino.se 1

- casino-sushi.gr – GR 1

- casino-swiper.es – ES 1

- casino-zet.gr – GR 1

- casino01-12-1 1

- casino06121 1

- casino1 48

- casino10 5

- casino11 4

- casino12 6

- casino13 6

- casino14 6

- casino15 6

- casino16 6

- casino17 7

- casino18 2

- casino19 6

- casino2 36

- casino20 1

- casino21 4

- casino22 5

- casino23 4

- casino24 2

- casino25 2

- casino26 1

- casino27 1

- casino28 2

- casino29 2

- casino3 31

- casino30 1

- casino31 2

- casino4 20

- casino5 14

- casino6 8

- casino7 5

- casino770 1

- casino8 8

- casino9 6

- Casinoandyou-casino.com_July 1

- Casinoandyou.pro 2

- casinobet1 7

- casinobet10 1

- casinobet12 1

- casinobet13 1

- casinobet14 1

- casinobet15 2

- casinobet16 1

- casinobet19 1

- casinobet2 2

- casinobet22 1

- casinobet24 1

- casinobet26 1

- casinobet27 1

- casinobet3 3

- casinobet4 3

- casinobet5 1

- casinobet6 1

- casinobet9 1

- casinobethall.es – ES 1

- casinoburan.gr – GR 1

- Casinocaspero.com 1

- casinodragonslots.no – NO 1

- Casinofambet.fr 1

- Casinogambloria.pl 1

- casinohrvatska 1

- Casinoly casino 2

- casinoNRGbet.co.uk – UK 1

- casinopistolo.es – ES 1

- Casinopistolo.pl 1

- casinoroobet.gr – GR 1

- casinos 6

- casinos-affiliate.com 1

- casinos-nongamstop.uk15 1

- casinos-online-europeos 1

- casinos-online-fuera-de-espana 1

- casinos1 1

- casinosinternacionalesonline.co.com 1

- casinoslot1 2

- casinoslot2 1

- casinoszondervergunning 1

- casinoways-games.com 1

- casinozet.gr – GR 1

- Casinozodiac.org 1

- casiny 1

- casiny1 1

- casono02123 1

- cataloghi di sposi per corrispondenza 1

- catalogo sposa per corrispondenza 2

- Catalogues de la commande par correspondance 1

- catГЎlogo de novias por correo 1

- cayyolutravel.com 1000 1

- cazino24 1

- cbaleixandre.es 1

- Cbd Oil For Sleep 124 3

- Cbd Oil For Sleep 810 2

- CCCCCCC 2

- cccituango.co 14000 1

- cdradvocacy.org 1

- cdu-ruegen.de 1

- celtabet- kiloalmaninyollari.net 1

- centralrest.ru 500 1

- centro cias 1

- CH 1

- chat bot names 4 2

- che cos'ГЁ il servizio di sposa per corrispondenza 1

- cheap college essay writing services 1

- cheap custom essay services 1

- cheap essay help online 1

- cheap essay writing service online 1

- cheap fast essay writing service 1

- cheap write essay 1

- cheap write my essay service 1

- cheeseyourway.ie Boomerang 1

- chickenroad 1

- chime chatbot 1 2

- christofilopoulou.gr 1

- chrstark.com 1

- chumak-mosokna.ru 500 1

- chytayemotut.com.ua 1

- Cialis 1

- circuitoestaciones.com.ar c5 1

- ciroblazevic.hr 1

- ciroillattaiodarmstadt-darmstadt.de 1

- cityoflondonmile1 1

- cityoflondonmile2 1

- cityoflondonmile3 1

- Cleobetra-casino.pro 1

- Cleobetracasino.info 1

- Clima-pro.de 1

- come acquistare una sposa per corrispondenza 1

- come fare una sposa per corrispondenza 1

- come funziona la sposa per corrispondenza 1

- come funzionano i siti di sposa per corrispondenza 1

- come ordinare la sposa per corrispondenza 1

- come preparare una sposa per corrispondenza 2

- come spedire una sposa 1

- Commandage mariГ©e Craigslist 2

- Commande de courrier Г©lectronique 10

- Commande par correspondance Definitiom 2

- Commande par courrier de la mariГ©e 2

- Commande par courrier lГ©gitime? 1

- commander par courrier une mariГ©e 1

- Commandez de la courrier mariГ©e rГ©elles histoires 2

- Commandez la mariГ©e rГ©el du site rГ©el 2

- Commandez par la poste pour de vrai? 1

- commanditГ© 5

- Comment acheter une mariГ©e par correspondance 1

- Comment commander de la mariГ©e 3

- Comment commander la commande par courrier mariГ©e 3

- Comment commander par la poste une mariГ©e 2

- Comment commander une mariГ©e par correspondance 2

- Comment commander une mariГ©e par correspondance russe 2

- Comment commander une mariГ©e russe mail 1

- Comment faire de la vente par la poste 5

- Comment faire une mariГ©e par correspondance 2

- Comment fonctionne la mariГ©e par courrier 2

- Comment fonctionne une mariГ©e par correspondance 2

- Comment fonctionnent la mariГ©e par courrier 3

- Comment fonctionnent les sites de mariГ©e par courrier 2

- Comment prГ©parer une mariГ©e par correspondance 2

- Comment prГ©parer une mariГ©e par correspondance Reddit 4

- Comment sortir avec une mariГ©e par correspondance 5

- Commout Mail Entre Russian Bride 1

- Como Registrarse Gratogana 715 1

- compra una sposa per corrispondenza 3

- comprar correo orden novia 1

- comprar una novia por correo 2

- Computers, Games 1

- Computers, Hardware 1

- correo de pedidos de la novia 1

- correo en orden cuestan novia 1

- correo en orden novia 2

- correo legГtimo ordenar sitios de novias reddit 1

- correo orden cupГіn de novia 1

- correo orden de citas de novias 1

- correo orden de cuentos de novias reddit 5

- correo orden de cuentos reales de novias 1

- correo orden novia real 1

- correo orden novia sitio real 1

- correo orden novia wiki 2

- correo orden novia wikipedia 1

- correo orden sitios de novias reddit 1

- correo para ordenar novia 2

- correo superior bride order web 1

- correo-pedido-novia 1

- cos'ГЁ la sposa per corrispondenza 4

- cos'ГЁ una sposa per corrispondenza 1

- cos'ГЁ una sposa per corrispondenza? 1

- cosmobetcasino.onlin 2

- cost-winemo.org 1

- costo medio della sposa per corrispondenza 1

- costo medio di una sposa per corrispondenza 1

- costo promedio de la novia del pedido por correo 1

- Coupon de mariГ©e par correspondance 2

- courrier des commandes de la mariГ©e 3

- Courrier pour commander la mariГ©e 3

- covid 2

- CoГ»t moyen d'une mariГ©e par correspondance 4

- CoГ»t moyen de la mariГ©e par correspondance 2

- crazy time IT 1

- crazy-time.br.com c4 1

- crazytimes.com.br c1 1

- creativeworkingplayground.com 1000 1

- Crypto2 1

- cryptocake.com 1

- Cryptocurrency exchange 4

- Cryptocurrency News 1

- csri-sc.org 1

- curacao-casino 1

- custom cheap essay 1

- custom essay cheap 1

- custom essay writers really cheap 1

- cz 1

- czbrandss 4

- cГіmo casarse con una novia por correo 1

- cГіmo enviar por correo a la novia 1

- cГіmo enviar por correo a una novia 1

- cГіmo hacer pedidos por correo novia 3

- cГіmo ordenar correo orden novia 2

- cГіmo pedir una novia rusa por correo 1

- cГіmo pedir una novia rusa por correo 5

- cГіmo preparar un correo orden novia reddit 2

- cГіmo preparar una novia por correo 1

- Daman game 1

- dating 3

- Dayz 1

- de_POST_3 1

- deberГa salir con una novia por correo 1

- dec_bh_common 2

- dec_nicebabylife.com 1

- dec_pb_common 2

- Definicija narudЕѕbe poЕЎte 2

- Definicija usluga za mladenke 1

- definisjon av postordre brud tjenester 3

- definizione dei servizi per la sposa per corrispondenza 1

- definizione sposa per corrispondenza 1

- detsadik36.rubonusi 500 1

- devrais-je sortir avec une mariГ©e par correspondance 1

- dicewise-casino.se 1

- Die Mail -Bestellungsbrautstelle 1

- Die Versandbestellbraut 5

- dinamobet – mabilnakit.com 1

- diplomrooma.com 1

- Disease & Illness, Breast Cancer 1

- Divaspin-australia.com 2

- Divaspin-casino.com 2

- Divaspin-casino.com_July 1

- Divaspincasino.org_July 1

- Djaro.pl 2

- Dk.trustpilot.com 1

- dkmarino.ru 2000 1

- do my essay for cheap 1

- do my essay for me cheap 1

- dogakentkres.com 2 1

- Dollycasino.live 3

- dorsetfalconrypark 1

- doubelochka.ru 10 1

- dove acquistare una sposa per corrispondenza 1

- dove compro una sposa per corrispondenza 1

- dove trovare una sposa per corrispondenza 1

- doy-ckazka.ru 1

- dozivivise.hr 2

- dragon money 1

- Dragonia-germany.com 1

- Dragonia-greece.com 2

- Dragonia-hungary.com 2

- Dragonia.pro 2

- dragonslots-casino.no – NO 1

- Dragonslotscasino.org 2

- Dragonslotscasino.pl 2

- draussen-magazin 1

- dripcasinoofficial.com 1

- drivein.hr 1

- drop sk, cz 1

- Drop-the-boss.net 3

- Droptheboss.org 3

- Duospincasino.net 4

- Durchschnittsalter der Postanweisung Braut 3

- Durchschnittspreis fГјr eine Versandbestellbraut 2

- Durchschnittspreis fГјr Versandbestellbraut 2

- Duselbstimberuf.de 1

- dutchbikeshop.ie Casinoly 2

- dxgamestudio 1

- DГ©finition de la mariГ©e par correspondance 1

- DГ©finition des services de vente par correspondance 1

- dГіnde comprar una novia por correo 1

- e-mail order bride 6

- E-Mail-Bestellung Braut 2

- e-post ordre brud 1

- e-post ordre brud nettsted anmeldelser 1

- E-posta SipariЕџi Gelin 1

- e-postorder brud 1

- Echte Versandbestellbraut -Sites 2

- Echte Versandbestellbrautwebsites 3

- Echte Versandungsbraut 1

- Echter Mail -Bestellung Brautservice 3

- Ecomretix.com 1

- eda-52.ru 500 1

- edad promedio de la novia del pedido por correo 1

- edeka-halmschlag.de 1

- edirectory.ie 1

- edu-solothurn.ch 1

- Education 1

- eeeeee 1

- Eine legitime Versandbrautbraut 3

- Eine Versandauftragsbraut 1

- ekte postordre brud nettsted 2

- ekte postordre brud nettsteder 1

- ekte postordre brudhistorier 1

- ekte postordrebrud 1

- elagentecine.cl 3

- elcolmaditodesarria.es 1

- electricnation 1

- En iyi posta sipariЕџi gelin Гјlkesi nedir 1

- En iyi posta sipariЕџi gelini sitesi nedir 1

- En iyi posta sipariЕџi gelini web siteleri 2

- en legitim postordrebrud 1

- En Д°yi Nominal Posta SipariЕџi Gelin Siteleri 1

- En Д°yi Posta SipariЕџi Gelin Гњlkeleri 1

- En Д°yi Posta SipariЕџi Gelin Ећirketi 1

- encontrar una novia por correo 1

- energycasino.eu.com – UK 1

- engelsegoksites 1

- English Casino 1

- er postordre brud verdt det 1

- er postordrebrud en ekte ting 1

- ergostasiooneirou.gr 1

- es la novia del pedido por correo algo real 1

- esc-privaterooms.de 1

- Esp Casino 1

- esposas de pedidos por correo 2

- essay cheap 1

- essay write for me 1

- essay writing for cheap 1

- essay writing on fast food 1

- ethnicitycelebration.ie MyStake 2

- etopechen.ru 500 1

- etsi minulle postimyynti morsian 1

- events-2011.rubonusi 500 1

- exbroke1 1

- exbroker1 1

- exness1 1

- exness2 2

- exness3 3

- exoneit.de 1

- expoescobar.com c1 1

- extension-autoroutes-non.ch 1

- extrade2 1

- F1.casinologowanie.net 1

- f1point0.com 1

- fadoinabox.pt 1

- Fairplay Online 824 1

- Fairspin-hu.net 2

- Faits de mariГ©e par correspondance 1

- Fambetkasino.de 1

- Fansbet Promo Code 631 2

- farma1 1

- farma3 1

- farma4 1

- farmacia 2

- farmacia1 1

- farmacia2 2

- farmaciadireta 1

- Fashion 7

- fckh.ru 1500 1

- fcommunity.ru 2

- felix-tropf 1

- femme de commande par correspondance 3

- festivalaki.gr 1

- ffnung-expert 1

- Finance, Personal Finance 2

- find a bride 6

- find a mail order bride 7

- find a wife 1

- find mail order bride 4

- find me a mail order bride 3

- Finden Sie eine Braut 1

- Finden Sie mir eine Versandbestellbraut 5

- finding a mail order bride 5

- findpolice.ru 700 1

- finn en brud 1

- finn en postordrebrud 3

- finn meg en postordrebrud 2

- finn postordrebrud 1

- finne en postordrebrud 1

- FinTech 5

- Fireballcasino-pl.pl 2

- Fireballcasino.de 2

- fiser.es 1

- fishingbaits.ru 2000 1

- fitago.ru 15 1

- flashdash-casino.com 1

- flashdash-nodepositbonus.com 1

- Fleksion.com 2

- fonbet-gr 1

- Food & Beverage, Cooking 1

- Food & Beverage, Wine 1

- foreign brides 5

- foreign brides dating 1

- Forex Trading 11

- fortunetiger 1

- Fqdns.net 2

- fr 2

- freedomcasino.se 1

- freshbet 1

- Fridayroll-casino.net_July 1

- Fridayroll.pro 2

- Fridayroll.pro_July 1

- Fridayrollkasino.de 1

- fruitslotpaly.com1 1

- Fun88 App Login 996 3

- gacor-slot 1

- galernaya20.ru 600 1

- Gambling 15

- Gambloriacasino.net 1

- Gambloriacasino.net_July 1

- Gambloriakasino.de 1

- game 2

- gameaviatorofficial.com 1

- gamebois.ch 1

- games 17

- gamestop 1

- gaming 1

- gangiborgodeiborghi 2

- gdje mogu dobiti mladenku za narudЕѕbu poЕЎte 1

- gdje mogu pronaći mladenku za narudžbu pošte 1

- Gegmany Casino 1

- Gegmany Casino2 1

- Gegmany Casino3 1

- Gelin SipariЕџ Posta AjansД± 1

- Gelin SipariЕџ PostasД± 1

- gembla 20.11 1

- geneeskunde 1

- generative ai application landscape 1 1

- generative ai in healthcare 1

- genetrix.es_casino-online-espana-legal 1

- genetrix.es_casino-online-europa 1

- gennaiapaidia.gr 1

- genomsnittspris för en postorderbrud 2

- German Casino2 2

- Gerçek Posta Siparişi Gelin Web Sitesi 1

- Gerçek posta siparişi gelini sitesi 1

- ggbet 1

- Ggbet.casinologowanie.net 101

- ghostwriter 1

- gjennomsnittlige postordre brudpriser 2

- gjennomsnittsalder for postordrebruden 1

- gjennomsnittspris for postordrebrud 3

- gjennomsnittspris pГҐ en postordrebrud 1

- gjennomsnittspris pГҐ en postordrebrud 2

- gjennomsnittspris pГҐ postordrebruden 2

- globalshopperu.com 1

- gode postordre brud nettsteder 3

- Golden Panda Casino Connexion 271 1

- good mail order bride sites 6

- good mail order bride website 4

- gorilla – four-paws.org.ua 1

- gosz-diplomas 1

- gpt 5 capabilities 5 1

- gradzasite.mk 1

- Grand National Wagering Offers & Free Of Charge Bets 2025 – 972 1

- Greece Casino 1

- grimme-aelling.dk 1

- Grm Betting 1

- Grm Casino 2

- GrosPlan.net 1

- Guerradelpacifico.org 2

- guide 9

- Gute Mail -Bestellung Brautwebsite 3

- gymsaludimagen.cl 2

- haciozkan.com 1000 1

- hackathome.pt 1

- haluan postimyynti morsiamen 1

- hanzbet.br.com1 1

- hashtagmafia.de 1

- hautarzt-rw.de 1

- Health & Fitness, Acne 1

- Health & Fitness, Depression 2

- Health & Fitness, Hair Loss 1

- Health & Fitness, Medicine 1

- Heatscasino.pl 1

- Heatskasino.de 1

- heiГџeste Mail -Bestellung Braut 1

- help to write my essay 1

- help-computers.ru 10 1

- herocolabs.com x 1

- hevesmegyehirdetoje.hu 1

- hipnosis para dejar las drogas 1

- Histoire de la mariГ©e par correspondance 2

- histoire vraie de la mariГ©e par correspondance 1

- histoires de la mariГ©e par correspondance rГ©elle 1

- Histoires de mariГ©e par correspondance reddit 1

- historia de la novia del pedido por correo 1

- historia om postorderbruden 1

- historia post order brud 1

- historiapostitilaus morsian 3

- historias de novias de pedidos por correo 2

- historias de novias de pedidos por correo real 1

- historie postordre brud 2

- historien til postordrebruden 1

- Historique de la mariГ©e par correspondance 2

- History -Mail -Bestellung Braut 2

- history mail order bride 5

- history of mail order bride 4

- historyohio.com 1

- hkb-jazz.ch 1

- holodok-pmr.ru 1000 1

- Home & Family, Gardening 1

- Home & Family, Home Security 1

- Home & Family, Landscaping 1

- Home & Family, Parenting 1

- hooplacomputer.hu2 1

- hospicehomejc.org 1

- Hot -Mail -Bestellung Braut 2

- hot mail order bride 4

- hot mail ordre brud 1

- Hot News 2

- hottest mail order bride 1

- hotteste postordrebrud 2

- how do mail order bride sites work 1

- how do mail order bride work 4

- how does a mail order bride work 4

- how does generative ai work 1

- how does mail order bride work 4

- how does mail order bride works 2

- how to buy a mail order bride 4

- how to date a mail order bride 3

- how to do a mail order bride 4

- how to do mail order bride 4

- How To Get Crypto Wallet 916 3

- how to mail order a bride 7

- how to mail order bride 3

- how to marry a mail order bride 3

- how to order a mail order bride 3

- how to order a mail russian bride 4

- how to order a russian mail order bride 7

- how to order mail order bride 3

- how to prepare a mail order bride 1

- how to prepare a mail order bride reddit 5

- hozsekrety.ru 1000 1

- html 1

- https.aviator.in 1

- https.www.dragontiger.in 1

- httpsbass-bet.eu.comhubonus – HU 1

- httpsbass-bet.eu.comhuslots – HU 1

- httpsbass-bet.eu.complmobile – PL 1

- httpsbass-bet.eu.complslots – PL 1

- httpsenergycasino.eu.comhubonuses – HU 1

- httpsenergycasino.eu.comhulogin – HU 1

- httpsenergycasino.eu.complbonuses – PL 1

- httpsenergycasino.eu.compllogin – PL 1

- httpsposido-casino.eu.comes – ES 1

- httpsposido-casino.eu.comeslogin – ES 1

- httpsposido-casino.eu.comesmobile – ES 2

- httpsposido-casino.eu.comfr – FR 1

- httpsposido-casino.eu.comfrmobile – FR 1

- httpsspinanga.eu.comesbonus – ES 1

- httpsspinanga.eu.comeslogin – ES 1

- httpsspinanga.eu.comitbonus – IT 1

- httpsspinanga.eu.comitlogin – IT 1

- httpswonaco.eu.comfrbonuses – FR 1

- httpswonaco.eu.comfrmobile – FR 1

- httpswonaco.eu.comhubonuses – HU 1

- httpswonaco.eu.comhumobile – HU 1

- Huffglu.com 1

- Hugo.casino 3

- Hugocasino-de.com 2

- Hugocasino-no.com 2

- huippuposti tilaus morsian 1

- huipputarjous morsiamen palvelut 1

- hundemesse-norderstedt.de 1

- hundesalon-gerlindeade.de 1

- hur beställer post brudarbete 1

- hur fungerar postorderbruden 2

- hur man beställer en postorderbrud 1

- hur man beställer en rysk postorderbrud 1

- hur man beställer postorder brud 1

- hur man gör postorder brud 1

- hur man köper en postorderbrud 1

- hva en postordrebrud 1

- hva er de beste postordrebrudstedene 1

- hva er den beste postordrebrudtjenesten 1

- Hva er en postordre brud 4

- hva er en postordrebrud 8

- hva er en postordrebrud? 4

- hva er postordrebrud 2

- hva er postordrebrud? 4

- hva er postordrebruden? 2

- hva er som postordrebrud 2

- hvor du kan kjГёpe en postordrebrud 1

- hvor finner jeg en postordrebrud 1

- hvor kan jeg finne en postordrebrud 1

- hvor kan jeg fГҐ en postordrebrud 1

- hvor kan jeg fГҐ en postordrebrud 2

- hvordan bestille en russisk brud 1

- hvordan date en postordrebrud 1

- hvordan du bestiller en postordrebrud 1

- hvordan du forbereder en postordre brud reddit 1

- hvordan du forbereder en postordrebrud 1

- hvordan du gjГёr postordrebrud 3

- hvordan du kan sende en brud pГҐ mail 3

- hvordan fungerer en postordrebrud 1

- hvordan fungerer postordrebruden 3

- hvordan kjГёpe en postordrebrud 1

- i 10 migliori siti di sposa per corrispondenza 2

- i 10 migliori siti web di sposa per corrispondenza 2

- i 5 migliori siti di sposa per corrispondenza 1

- i migliori paesi per ottenere una sposa per corrispondenza 1

- i migliori paesi per una sposa per corrispondenza 2

- i migliori siti di sposa per corrispondenza 2

- i migliori siti di sposa per corrispondenza. 2

- i migliori siti web per la sposa per corrispondenza 1

- i posti migliori per ricevere la sposa per corrispondenza 1

- i siti della sposa con le migliori offerte 1

- i want a mail order bride 7

- icecasino-greece.com – GR 1

- icecasinoportugal.com – PT 1

- icestupa1 1

- icestupa11 1

- icestupa2 2

- icestupa3 1

- icestupa4 4

- icestupa6 1

- icestupa7 1

- icestupa9 1

- Ich möchte eine e Mail -Bestellung Braut 2

- id-1xbet.com 2

- IGAMING 10

- igry 1

- igry-nardy.ru 240 1

- ihnk.ru 700 1

- il sito della sposa per corrispondenza 2

- Ilifewire.com 2

- illiya 1

- in cerca di matrimonio 1

- inbet-casino.gr – GR 1

- inbetcasino.gr – GR 1

- independentcommissionfees 1

- india22bet.com 1

- indon-1xbe1.com 2

- Indonesia Casino 6

- Indonesia Casino1 8

- Indonesia Casino4 2

- Indonsia Slot Gacor 2

- Indonsia Slot Gacor2 4

- Industrie des mariГ©es par correspondance 3

- infinity-gr.com – GR 1

- infinitycasino-gr.net – GR 1

- infinitycasino-greece.com – GR 1

- info 14

- infopot.ru 2500 1

- Informacije o mladenki 2

- informaciГіn de la novia del pedido por correo 2

- Informations sur les mariГ©es par correspondance 4

- inovirajprofitiraj.hr 2 1

- inquisitivereader.com z1 1

- inquisitivereader.comapp z2 1

- insure 1

- internasjonal postordrebrud 2

- international mail order bride 4

- Internationale Mail -Bestellung Braut 2

- Internet Business, Blogging 1

- Internet Business, Domains 1

- Internet Business, Ecommerce 2

- Internet Business, Email Marketing 1

- Internet Business, Security 1

- Interracial Mail -Bestellung Braut 1

- interracial mail order bride 6

- interracial postordre brud 1

- Interwetten Casino Schweiz 1

- Interwetten Österreich – Offizielle Website 1

- ireland2040.ie 1Bet 1

- Irwin-pt.com 1

- Irwin-pt.com_July 1

- is mail order bride a real thing 3

- is mail order bride real 4

- is mail order bride safe 1

- is mail order bride worth it 6

- iskonstrukcije.hr 1

- iskra-guitars.ru 1

- islamicpersia.org 1

- Ist die Versandbraut real 1

- Ist Versandbestellbraut eine echte Sache 1

- Ist Versandbestellbraut es wert? 1

- Ist Versandbestellbraut sicher 1

- IT Vacancies 1

- IT Вакансії 1

- Ita Casino 2

- Italy Betting 1

- Italy Casino2 1

- Italy Casino3 1

- italyanmutfagihaftasi.com 1 1

- italywinnita 1

- ivermectin 1

- ivermectina 1

- Ivermectine 1

- ivibet-casino.gr – GR 1

- izzi 2

- Jak Wypłacić Pieniądze Z Slottica Casino Casino Slots Demo – 153 1

- japan-bcgame.com 1

- japan-greece-business.gr 1

- jardiance 1

- jaya9 2

- jaya91 2

- jaya92 2

- jbcasino2 1

- Je li Mail narudЕѕba mladenka stvarna 1

- Je li mladenka narudЕѕba prava prava stvar 1

- Je li narudЕѕba poЕЎte sigurna 1

- Je veux une mariГ©e par correspondance 3

- Jeetbuzz Live 327 1

- jeg vil ha en postordrebrud 1

- jetbahis – gard.org.tr 1

- Jetton 7

- Jeux 1

- jk-yagoda.com.ua 1

- Jodah.org 2

- JojoBet 1

- Jojobet 2024 Many Characteristics Only In Turkish Sbs" – 345 4

- jokerbet – hakankaraarslan.com.tr 1

- jomboydon.uz 1

- Joomy.net 1

- jos-trust 1

- joy-in-iran.de 1

- jugabet CL – chile-jugabet.cl 1

- Kako kupiti mladenku za narudЕѕbu poЕЎte 1

- Kako naruДЌiti mladenku za narudЕѕbu poЕЎte 1

- Kako naruДЌiti rusku narudЕѕbu poЕЎte 1

- Kako pripremiti mladenku za narudЕѕbu poЕЎte 1

- Kako radi mladenka za narudЕѕbu poЕЎte 1

- Kako radi na narudЕѕbi Mail 2

- Kako radi narudЕѕbe za narudЕѕbu poЕЎte 2

- Kakva narudЕѕba poЕЎte 1

- Kaloxdigital.com 2

- kampo-view.com 1

- Kann ich eine Versandungsbraut bekommen, wenn ich bereits verheiratet bin? 1

- Kasinospinbara.de 1

- Kasyno online Poland 3

- Kasyno Slottica Kod Promocyjny Pragmatic Tak Szybko – 405 1

- kasynonaprawdziwepieniadze 1

- kaszino 1

- kaszino1 2

- Kauf einer Mail -Bestellung Braut 4

- Kaufen Sie eine Mail -Bestellung Braut 2

- kazan99.ru 1000 1

- kazino-onlayn-reyting-luchshih.xyz 2 1

- kazino-onlayn-reyting.xyz 2 1

- kazino1 3

- kazino2 1

- kgskouskosh3.ru 4000 2

- khelo24betoficcial.com 1

- khl.hr 2 1

- kicksite.pl 1

- kinbet-casino.at 1

- kjГёp postordrebrud 2

- kjГёper en postordrebrud 3

- klarna 1

- klgsystel.com 1

- Klubnika 1

- Klubnika 1 1

- koispinscasino.co.uk 1

- komod-testfeld 1

- Korea 1

- kriptokaszino 1

- kromatografi2023.org 1 1

- kshhaveservice.dk 1

- Kto Cassino Online 5 3

- kudo-mo.ru 300 1

- kuinka ostaa postimyynti morsiamen 1

- kuinka postimyynti morsiamen 1

- kuinka päivämäärä postimyynti morsiamen 1

- kuinka tilata postia venäläinen morsian 2

- kuinka tilata postimyynti morsiamen 1

- kulisbet – beyogluogretmenevi.com 1

- kunstraumwinterthur.ch 1

- kymmenen suosituinta postimyyntiä morsiamen verkkosivustoa 1

- La commande par correspondance en vaut-elle la peine 3

- La courrier Г©lectronique en vaut la peine? 3

- la mariГ©e par correspondance 2

- La mariГ©e par correspondance en vaut la peine 1

- La mariГ©e par correspondance en vaut la peine 3

- La mariГ©e par correspondance est-elle sГ»re 2

- la migliore corrispondenza per corrispondenza della sposa 1

- la migliore sposa per corrispondenza di sempre 2

- la sposa per corrispondenza ne vale la pena? 2

- lailliset postimyynti morsiamen verkkosivustot 1

- lailliset postimyyntiyritykset 1

- laopcion.com.co 1

- larocca.cl 6

- larocca.clbonos-sin-deposito 2 1

- larosa22.es 1

- ldmusical.com.mx 1

- Le site de la mariГ©e par correspondance 3

- Legale Versandhandel Seiten für Bräute 4

- leggit mail order bride sites 4

- leggit postordre brud nettsteder 3

- legiano 1

- legiano casino opinie 1

- legiano casino review 1

- Legit Mail NarudЕѕba mladenka 2

- Legit Mail narudЕѕbe mladenke 1

- legit mail order bride 7

- legit mail order bride service 7

- legit mail order bride site 4

- legit mail order bride sites 4

- legit mail order bride sites reddit 4

- legit mail order russian bride 5

- legit postimyynti morsiamen palvelu 1

- legit postimyynti morsiamen sivustot 1

- legit postimyynti morsian 2

- legit postorder brud webbplatser reddit 2

- legit postorder ryska bruden 1

- legit postordre brud 3

- legit postordre brud nettsteder 1

- legit postordre brudtjeneste 1

- legitim postorder brud 1

- legitim postorder brud webbplatser 1

- legitim postorder brudens webbplats 2

- legitim postorder brudföretag 2

- legitim postordre brudsted 1

- legitim postordrebrud 4

- legitimale Mail -Bestellung Braut 5

- legitimate mail order bride 4

- legitimate mail order bride companies 9

- legitimate mail order bride services 5

- legitimate mail order bride site 4

- legitimate mail order bride sites 7

- legitimate mail order bride website 3

- legitimate mail order bride websites 4

- legitime Mail -Bestellung Braut Site 2

- legitime Mail -Bestellung Brautdienste 3

- legitime Mail bestellen Brautunternehmen 1

- Legitime Mail bestellen Brautwebsite 2

- legitime Mail bestellen Brautwebsites 2

- legitime postordre brudtjenester 1

- legitime postordrebrudesider 1

- legitime Versandbestellbraut 2

- legitime Versandbestellbrautstandorte 3

- legitimer Versandauftragsbrautservice 2

- legitimert postordre brudtjeneste 1

- Legitimna narudЕѕba poЕЎte 1

- Legitimne web stranice za mladenke 1

- legitimt postordrebrud nettsted 1

- Legitimte -Mail -Bestellung Brautservice 2

- legitimte mail order bride service 2

- legitimte postorder brudtjänst 1

- legittima vendita per corrispondenza sposa 1

- legittimare il servizio di sposa per corrispondenza 1

- legjobbmagyarcasino.online 1

- lekarnaskupaj 1

- lekarnaskupaj.si 1

- lemoncasino-hu.com – HU 1

- Lemoncasino.net_July 1

- lenovo-smart.ru 2000 1

- leonov16.ru 500 1

- Les sites de mariГ©e par correspondance lГ©gitimes 5

- lesbian mail order bride 8

- lesbian mail order bride reddit 3

- Lesbienne Mail Commande Bride Reddit 4

- lesbische Versandbestellung Braut Reddit 2

- lesbisk postorder brud 1

- lesbisk postordre bruden reddit 3

- lesbisk postordrebrud 1

- letar efter äktenskap 2

- letsjackpot-casino.com 1

- Lev 2

- Limere.pl 2

- Line Bet 742 2

- linebet-uzbekistan.org 1

- Linkayz.com 1

- links_dealer_liech 1

- links_dealer_luxem 2

- links_dealer_madagas 2

- links_dealer_malawi 3

- links_dealer_maldives 2

- links_dealer_mali 1

- links_dealer_malta 4

- links_dealer_mauritus 4

- list of best mail order bride sites 4

- Liste der besten Mail -Bestell -Braut -Sites 4

- Liste des meilleurs sites de mariГ©es par correspondance 2

- liste over beste postordre brudsider 2

- livecasinoz 2

- loainnhoteles.com.mx c2 1

- lokalenizbor.mk 1

- Lol Worlds 2024 Betting Probabilities Teams Tips On How To Bet" – 267 4

- looking for a mail order bride 4

- looking for marriage 2

- los 10 mejores sitios para novias por correo 1

- los 10 principales sitios web de novias por correo 2

- los 5 mejores sitios para novias por correo 1

- LotoClub1 1

- lovepang.ie Malina 1

- ltrading17 1

- luchshie-casino-rajting ancorallZ dp 1

- luckhome.ru 2000 1

- Lucky Jet 1win 515 3

- lucky-star1 1

- lucky-stars 1

- lucky777star.in 1

- luckystar-casino.xyz 1

- luckystar-official.com 1

- luckystar777.org 1

- luckystar777club.org 1

- luckystaraviator.onlin 1

- luckystarcasino 1

- luckystarcasino.info 1

- luckystarcasinoindia7.org 1

- lyrica 2

- löytää morsian 1

- Mad-casinos.com 4

- magicofstone.ru 500 1

- magicwinlogin.com 1

- Magius-kasyno.pl 3

- Magiuscasino.co 4

- Magiuskasino.de 1

- magyar-online-casino 1

- Mail -Bestellung Braut 5

- Mail -Bestellung Braut -Websites ?ГјberprГјfen 4

- Mail -Bestellung Braut Datierung 5

- Mail -Bestellung Braut definieren 3

- Mail -Bestellung Braut echt 5

- Mail -Bestellung Braut es wert ist 2

- Mail -Bestellung Braut legitim 4

- Mail -Bestellung Braut zum Verkauf 1

- Mail -Bestellung Brautagentur mit dem besten Ruf 4

- Mail -Bestellung Brautagenturen 1

- Mail -Bestellung Brautbewertung 4

- Mail -Bestellung Brautdating Site 3

- Mail -Bestellung Brautdienste 1

- Mail -Bestellung Brautdienste Definition 1

- Mail -Bestellung Brautindustrie 1

- Mail -Bestellung Brautkatalog 5

- Mail -Bestellung Brautkataloge 2

- Mail -Bestellung Brautkupon 2

- Mail -Bestellung Brautservice 2

- Mail -Bestellung Bride Agency Reviews 3

- Mail an die Braut bestellen 4

- Mail auf Bestellung Braut 6

- Mail bestellen Braut Arbeit? 2

- Mail bestellen Braut Craigslist 2

- Mail bestellen Braut echte Geschichten 1

- Mail bestellen Braut gute Idee? 3

- Mail bestellen Braut legitim 4

- Mail bestellen Braut legitim? 3

- Mail bestellen Braut Reales Standort 2

- Mail bestellen Braut Reveiw 1

- Mail bestellen Braut Websites Bewertungen 4

- Mail bestellen Braut Websites Reddit 1

- Mail bestellen Braut Wikipedia 1

- Mail bestellen Brautartikel 7

- Mail bestellen Brautgeschichten 4

- Mail bestellen Brautgeschichten Reddit 1

- Mail bestellen Brautinformationen 3

- Mail bestellen Brautlender 1

- Mail bestellen Brautstandorte legitim 4

- Mail bestellen Brautwebes Reddit 1

- Mail bestellen Brautwebsite 3

- Mail bestellen eine Braut 3

- Mail bestellen Frauen 2

- mail bride order 2

- mail brudbeställning 2

- Mail dans l'ordre de la mariГ©e 3

- Mail dans l'ordre du coГ»t de la mariГ©e 1

- Mail dans la dГ©finition de la mariГ©e 6

- mail for brudekostnad 1

- mail for ГҐ bestille brud 2

- mail i ordning brud kostar 1

- mail i rekkefГёlge brud 2

- mail i rekkefГёlge bruddefinisjon 2

- Mail in der Bestellung Brautdefinition 2

- mail in order bride 5

- mail in order bride cost 3

- mail in order bride definition 2

- Mail Mail 1

- Mail narudЕѕba mladenka definira 1

- Mail narudЕѕba mladenka stvarna 1

- Mail narudЕѕba mladenka vrijedi 1

- Mail narudЕѕba mladenka vrijedi? 1

- Mail narudЕѕbe mladenke 1

- Mail narudЕѕbe mladenke web stranice Reddit 1

- Mail narudЕѕbe mladenke za stvarno 3

- Mail narudЕѕbe za mladenke legitimne 2

- Mail narudЕѕbena agencija s najboljom reputacijom 1

- Mail on Order Bride 7

- mail order a bride 3

- mail order bride agences 4

- mail order bride agencies 5

- mail order bride agency 7

- mail order bride agency reviews 4

- mail order bride agency with the best reputation 7

- mail order bride articles 5

- mail order bride catalog 10

- mail order bride catalogs 6

- mail order bride catalogue 5

- mail order bride countries 4

- mail order bride coupon 3

- mail order bride craigslist 4

- mail order bride dating 4

- mail order bride dating site 8

- mail order bride dating sites 2

- mail order bride define 4

- mail order bride definitiom 3

- mail order bride definition 2

- mail order bride facts 7

- mail order bride faq 5

- mail order bride for real 3

- mail order bride for real? 4

- mail order bride for sale 8

- mail order bride good idea? 5

- mail order bride industry 8

- mail order bride info 4

- mail order bride information 4

- mail order bride legit 3

- mail order bride legit sites 3

- mail order bride legit? 4

- mail order bride real 7

- mail order bride real site 7

- mail order bride real stories 2

- mail order bride reveiw 7

- mail order bride review 6

- mail order bride reviews 5

- mail order bride service 6

- mail order bride services 3

- mail order bride services definition 5

- mail order bride sites 4

- mail order bride sites legitimate 4

- mail order bride sites reddit 3

- mail order bride sites review 3

- mail order bride stories 8

- mail order bride stories reddit 3

- mail order bride story 6

- mail order bride website 6

- mail order bride website reviews 6

- mail order bride websites 3

- mail order bride websites reddit 5

- mail order bride websites reviews 4

- mail order bride wiki 3

- mail order bride wikipedia 5

- mail order bride work? 2

- mail order bride worth it 3

- mail order bride worth it? 5

- mail order sposa informazioni 1

- mail order wife 6

- mail order wives 4

- mail ordina le informazioni sulla sposa 2

- mail på beställning brud 1

- mail pГҐ bestilling brud 2

- mail to order bride 5

- mail-order bride 6

- Mail-Order-Braut 6

- mail-order-bride 8

- Mail. Bride Legit 2

- Mailbrautbestellung 3

- maisondecharme.ru 1000 1

- makaleozgunluktesti.com 500 1

- Malay Casino 1

- manaki.mk 1

- mariobet – merveninpenceresi.com 2

- marios-grosser-traum.de 1

- mariГ©e par correspondance 1

- mariГ©e par correspondance 7

- mariГ©e par correspondance chaude 1

- mariГ©e par correspondance dГ©finir 4

- mariГ©e par correspondance en ligne 4

- mariГ©e par correspondance internationale 4

- mariГ©e par correspondance interraciale 2

- mariГ©e par correspondance lesbienne 3

- mariГ©e par correspondance lГ©gitime 4

- mariГ©e par correspondance pour de vrai 2

- mariГ©e par correspondance reveiw 5

- mariГ©e par correspondance rГ©elle 3

- mariГ©e par correspondance Г vendre 2

- mariГ©e par la poste d'historique 1

- marvel-bet-bd.com 1

- maslakotokurtarici.com 1000 1

- mazda-avtomir.kz 1

- mbousosh10.ru 4-8 1

- mdash.ru 300 1

- medelålder för postorderbruden 1

- mediapedia.mk 1

- medic 2

- medisource.ru 500 1

- medmind.ru 4-8 1

- mega168bet.com 1

- Megarich-casino.net 1

- Meilleur endroit pour la mariГ©e par correspondance 1

- Meilleur endroit pour obtenir la mariГ©e par correspondance 3

- Meilleur endroit pour obtenir une mariГ©e par correspondance 2

- Meilleur pays de mariГ©e par correspondance 1

- Meilleur pays pour la mariГ©e par correspondance 5

- Meilleur pays pour trouver une mariГ©e par correspondance 2

- Meilleur service de mariГ©e par correspondance 3

- Meilleur site Web de mariГ©e par correspondance 1

- Meilleure agence de mariГ©e par correspondance 1

- Meilleure mariГ©e par correspondance 2

- Meilleure mariГ©e par correspondance de tous les temps 5

- Meilleure Г©pouse de vente par correspondance de rГ©putation 3

- Meilleurs avis sur les sites de mariГ©e par correspondance 2

- Meilleurs endroits pour la mariГ©e par correspondance 3

- Meilleurs endroits pour obtenir la mariГ©e par correspondance 2

- Meilleurs lieux de mariГ©e par correspondance 3

- Meilleurs pays de la mariГ©e par correspondance 3

- Meilleurs sites de mariГ©e par correspondance 1

- Meilleurs sites de mariГ©s par correspondance rГ©el 4

- Meilleurs sites Web de la mariГ©e par correspondance 2022 1

- Meilleurs sites Web de mariГ©e par correspondance lГ©gitime 2

- Meilleurs sites Web de mariГ©es par correspondance reddit 3

- mejor correo orden novia agencia reddit 1

- mejor correo orden sitios web de novias reddit 1

- mejor lugar para recibir pedidos por correo novia 1

- mejor lugar para recibir un pedido por correo novia 1

- mejor orden de correo novia 1

- mejor paГs para encontrar la novia del pedido por correo 1

- mejor paГs para encontrar una novia por correo 1

- mejor paГs para la novia del pedido por correo 1

- mejor paГs para pedidos por correo novia reddit 1

- mejor reputaciГіn correo orden novia 2

- mejor sitio de novias por correo 1

- mejores lugares para la novia por correo 2

- mejores lugares para novias por correo 1

- mejores lugares para recibir pedidos por correo novia 1

- mejores paГses para una novia por correo 2

- mejores sitios para novias por correo 1

- mejores sitios web de novias por correo 2022 1

- mejores sitios web de novias por correo legГtimo 2

- melbet-app.pro2 1

- melbetcanada.org3 1

- menoumethess.gr 1

- Mericola.com 2

- meritking 2 1

- metabet18 2

- miglior ordine di posta elettronica siti web sposa reddit 1

- miglior ordine di posta sposa sito reddit 4

- miglior ordine postale agenzia sposa reddit 1

- miglior ordine postale sposa paese 1

- miglior paese per trovare una sposa per corrispondenza 1

- miglior servizio di sposa per corrispondenza 2

- miglior sito per sposa per corrispondenza reale 2

- miglior sito web per la sposa per corrispondenza 2

- miglior sito web per trovare una sposa per corrispondenza 1

- migliore compagnia di sposa per corrispondenza 1

- migliori compagnie di sposa per corrispondenza 1

- migliori recensioni per i siti della sposa 2

- migliori siti di sposa per corrispondenza 2

- miglioricasinononaams.com 1

- mikä on postimyynti morsiamen palvelut 1

- mikä on postimyynti morsian 2

- mikä on postimyynti morsian? 1

- mikä postimyynti morsian 1

- MINDES MINDES Web lokacije. 1

- Minebitcasino.com 2

- Minebitcasino.com_July 1

- Minedrop-slot.com 2

- mines.br.compt-br c1 1

- minimitalletus-kasinot.org 1

- minimumstorting 1

- Miodwarzywa.pl 2

- mireillelebel.de 1

- missionaguafria.com 1

- Missoletes.com_July 1

- mistä löytää postimyynti morsiamen 1

- mistä ostan postimyynti morsiamen 1

- miten postimyynti morsiamen toimii 1

- Mix Porn 1

- Mjesto za mladenku s gornjom poЕЎtom 1

- mjm-communication.com 1

- mladenka 3

- mladenka s najviЕЎe poЕЎte 1

- mladenke za mladenke mladenke 2

- Mma Bet Download 361 3

- moglie per corrispondenza 1

- montecatini.cl 2

- morsiamen postimyynti 1

- morsiamen tilausposti 1

- mortkombx.ru 1

- mosbet-1 1

- mosgorduma24.ru 500 1

- Mostbet 6

- Mostbet 2 1

- Mostbet 3 1

- Mostbet Kz 867 3

- Mostbet Mobile Software Review Android & Ios Perfect Experience – 645 4

- Mostbet Mundial 2022 Is Metrodeal Safe In The Korea? How Can Metrodeal Function?" – 31 4

- MostBet Schweiz Website 1

- mostbet Wagering On The App Store" – 90 4

- mostbet-2 1

- mostbet-4 2

- mostbet-5 1

- mostbet-official.co.in 1

- mostbet-oynash.org 1

- mostbet-registration-az 1

- mostbet1 2

- mostbet2 4

- mostbet3 4

- mostbet4 1

- mostbetuzcasino.com 1

- MoЕѕete li naruДЌiti mladenku 2

- msgbc2021 1

- municasablanca.cl 2

- mvclinic.ru 2 1

- my-1xbet.com 1

- my-busines.ru 10 1

- my-busines.ru 150 1

- mybrtracing 1

- myownconference 1

- Myriad-Play.co.uk – UK 1

- mystakecasino.ch 1

- naalelimitedcasinos 1

- Najbolja mjesta za mladenku za narudЕѕbu poЕЎte 1

- Najbolja narudЕѕba Mail ikad 1

- Najbolja narudЕѕba poЕЎte 1

- Najbolja narudЕѕba za mladenku 1

- Najbolja narudЕѕba za mladenku Reddit 1

- Najbolja reputacija narudЕѕbe mladenke 2

- Najbolja web stranica za mladenku 1

- Najbolja web stranica za pronalaЕѕenje mladenke za narudЕѕbu poЕЎte 2

- Najbolja zemlja za mladenku za narudЕѕbu poЕЎte 1

- Najbolja zemlja za pronalaЕѕenje mladenke za narudЕѕbu poЕЎte 1

- Najbolje mjesto za dobivanje mladenke za narudЕѕbu poЕЎte 2

- Najbolje narudЕѕbe mladenke 1

- Najbolje narudЕѕbe za mladenke 2022 1

- Najbolje narudЕѕbe za mladenke recenzije 1

- Najbolje web stranice za mladenke prave poЕЎte 2

- najbolje zemlje za mladenku za narudЕѕbu poЕЎte 1

- Najtoplija narudЕѕba poЕЎte 1

- narudЕѕba poЕЎte mladenka wikipedia 2

- narudЕѕbe maila za mladenke reddit 1

- NaruДЌivanje poЕЎte FAQ FAQ 1

- NaruДЌivanje poЕЎte mladenka Real web mjesto 1

- NaruДЌivanje poЕЎte mladenke 3

- NaruДЌivanje poЕЎte stvarne priДЌe 1

- nastolki18.ru 10 1

- nastya 1

- nationalbet-casino.com 1

- nationalnurse.org 1

- navegar por correo orden novia 1

- nbanews.ru 500 1

- nbetclic.com 1

- Neospin.vip 1

- Netherlands 1

- Netherlands Casino 6

- Netherlands Casino1 2

- Neue Casinos Schweiz 2025 1

- Nevjesta narudЕѕba poЕЎte 1

- Nevjesta za internetsku poЕЎta 2

- Nevjesta za narudžbu vruće pošte 1

- New 12

- New folder 3

- New Post 1

- News (5,834)

- News top 2

- news-top 5

- NEWSTOP 1

- newz 1

- nexoriahub.work 1

- nikosxeiladakis.gr 1

- nine-gr.com – GR 1

- Nine9casino.net 1

- ninecasino-greece.com – GR 1

- Ninecasino-pt.net 1

- ninecasinoofficial.de 1

- Ninecasinoonline.net 1

- ninlay.eu.com – UK 1

- NL 1

- NL_post 1

- No comments 1

- nobullchallenge 1

- nodeposit 1

- Nomad 7

- nominicasino-si.com – SI 1

- nongamstop-casinos 1

- Norwegian Casino 1

- Norwen Casino 1

- nov_chinabackpacker 1

- nov1 2

- nov2 1

- nov5 1

- nov7 1

- novia de pedidos por correo 2

- novia mГЎs caliente por correo 1

- novibet-greece.com 1

- nowe-kasyna 1

- NRGbetcasino.co.uk – UK 1

- nv casino 2

- NV Casino Bonus 1

- NV Casino Schweiz Bewertungen auf TrustPilot 1

- Nv-kasino.com 2

- Nv-kasyno.net 3

- nzzpuss.hr 1

- Oceanspin.pro 1

- Oceanspin.pro_July 1

- Oceanspincasino.org_July 1

- oct3 1

- officialpinupcasino.com 1

- Offizielle Interwetten-Website 1

- Offizielle Website des Kingmaker Casinos in der Schweiz 1

- ogrn-inn.ru 4-8 1

- oikeat postimyynti morsiamen sivustot 1

- oikeat postimyynti morsiamen verkkosivustot 1

- oja22.de 1

- okggpoker.lol 1

- okonlineplay.live 1

- olympecasinos.com 1

- omegle 1

- on postimyynti morsian sen arvoinen 1

- ondr.pt 1

- Online -Mail -Bestellung Braut 2

- Online Casino Australia Real Money 631 1

- online casino buitenland 1

- online casino Neteller 1

- online casino paysafecard 1

- online gokken buitenland 2

- online mail order bride 3

- online postordre brud 1

- online-slots 1

- onlinecasino1 1

- onlinecasinomonobrands 1

- onlinecasinopolska 1

- onlysushi-club.ru 500 1

- oooat.ru 1

- opencfd 1

- orden de correo de la industria de la novia 2

- orden de correo de la novia 1

- orden de correo de las agencias de la novia 2

- orden de correo definiciГіn de novia 1

- orden de correo electrГіnico novia 2

- orden de correo internacional novia 1

- orden de correo legГtimo novia 2

- orden de correo lГ©sbico novia 4

- orden de correo novia 4

- orden de correo real novia 1

- ordenar por correo hechos de novia 2

- order essay cheap 1

- ordine postale sposa definire 1

- ordine postale sposa definizione 1

- organismosathinas.gr 1

- originalidiplas 1

- ortokonovalov.ru 120 1

- orzuniyat.com 1

- Oscarspinkasyno.pl 1

- ostaa postimyynti morsiamen 1

- oГ№ acheter une mariГ©e par correspondance 5

- OГ№ puis-je acheter une mariГ©e par correspondance 2

- oГ№ puis-je trouver une mariГ©e par correspondance 1

- oГ№ trouver une mariГ©e par correspondance 3

- p0cketopti0n.com 1

- p0kerdom.wiki 1

- Pablic 2

- padişahbet – spoura.com 1

- pages 11

- palmsbetcasino.gr – GR 1

- paras maa löytää postimyynti morsiamen 2

- paras paikka saada postimyynti morsiamen 1

- paras postimyynti morsiamen maa 1

- paras postimyynti morsiamen palvelu 2

- paras postimyynti morsiamen sivusto 1

- paras postimyynti morsiamen verkkosivusto 1

- paras postimyynti morsiamenvirasto reddit 1

- paras sivustopostitilaus morsian 1

- paras todellinen postimyynti morsiamen sivusto 1

- paras verkkosivusto löytääksesi postimyynti morsiamen 1

- parhaat maat saada postimyynti morsiamen 1

- parhaat oikeat postimyynti morsiamen sivustot 1

- parhaat paikat saada postimyynti morsiamen 2

- parhaat postimyynti morsiamen maat 2

- parhaat postimyynti morsiamen paikat 2

- parhaat postimyynti morsiamen sivustot 1

- parhaat postimyynti morsiamen verkkosivustot 2022 1

- Parimatch Live 629 3

- parimatch-aviator.in x 1

- parteineueliberale.de 1

- partner2b 1

- Party Casino 373 3

- Party Casino Bono Sin Deposito 339 3

- pass4sure 1

- patoaraya.cl 1

- patridiots.com 1

- pauzazapregled.mk 1

- pay for essay papers 1

- pay for my essay 1

- pay someone to write my essay for me 1

- Pays des mariГ©es par correspondance 4

- pedido por correo novia en venta 1

- pedidos por correo de catГЎlogos de novias 1

- pedidos por correo de reseГ±as de agencias de novias 1

- pedidos por correo de reseГ±as de novias 1

- pedidos por correo sitios de novias legГtimos 1

- Penaltyshootout-slot.fr 1

- Pensionheide.de 1

- per corrispondenza 1

- per corrispondenza sposa reveiw 2

- per corrispondenza sposa storia 1

- per corrispondenza sposa wiki 1

- pereezd.pl.ua 1

- performances-recherche.ch 1

- persona-maslovka.ru 300 1

- petzanet.hr 2 1

- pflegedienst-g-a-und-b.de 1

- pg-slot 1